The federal government recently passed another omnibus stimulus bill. This one has a few interesting provisions that people in (or pursuing) FIRE should be aware of for their planning this year.

$1,400 stimulus checks

All the big headlines are on the $1,400 stimulus checks available to income-qualified taxpayers and their dependents. Most people have already received these payments based on the income reported in their most recent tax return. For those whose income was too high in 2019 (or 2020, if they filed their taxes early), but expect to have qualifying income in 2021, the $1,400 will be available as part of their tax refund in 2022.

This stimulus payment has a very narrow phase-out range ($5,000 for single people, $10,000 for married couples). If you didn’t receive a payment because your 2019/2020 income was too high, but you could potentially engineer your income to be below the line this year, that could be a worthwhile thing to do.

Child tax credit

The child tax credit was increased this year. It used to be $2,000 per qualifying child, now it’s $3,000 ($3,600 for kids under 6). More importantly for FIREd families, the credit is now fully refundable, meaning you can get the full amount regardless of how much other income you have.

Previously a portion of the $2,000 was refundable, but only for people who had a certain amount of work income. It was fully non-refundable for FIREd individuals whose income came entirely from investments. As capital gains and dividends have a pretty big range where they’re taxed at 0%, someone getting most of their income from a taxable brokerage account might not have realized any benefit from the child tax credit at all!

For that reason it used to be advantageous to realize some regular income (such as from Roth conversions) to maximize the child tax credit. The tax credit would cancel out the first $2,000 of tax per qualifying kid, creating a pretty big income range with zero net tax liability. This is no longer the case. Now someone with no income starts out with a $3,000 refund per kid, and regular income will start chipping away at this refund beginning with the first dollar above the standard deduction.

This change to the child tax credit currently applies to the year 2021 only, but leading Democrats have stated their intention to extend it to future years as well. Stay tuned.

Earned income credit

The earned income credit has been a long-standing feature of the tax code, giving low-income working families a bit of a financial boost. It is only available at lower incomes, and only to families without much investment income. The investment income limit is a hard cutoff: $1 below the limit and you get the full earned income credit; $1 above and you get nothing. The idea was to target the credit specifically at people without much wealth, to exclude low-income millionaires who aren’t really working for a living anymore.

This investment income limit was previously $3,650 per year. As VTSAX will throw off roughly 2% in dividends alone, a FIREd family with a six-figure balance in taxable brokerage accounts was unlikely to qualify for the credit even if they had a bit of barista-FIRE-style work income. The stimulus bill raises this limit to $10,000 of investment income. There’s no end date attached to this change. This makes the earned income credit much more attainable to those FIREd parents with a bit of income coming in from a part-time job.

ACA premium tax credits

The bill also increases premium tax credits for people buying their health insurance from their local ACA marketplace. The cliff at 400% of the poverty level is eliminated, allowing the tax credit to phase out gradually until premiums hit 8.5% of a person’s income.

At the low end of the scale, the net premium for the second-cheapest silver plan (and any cheaper plan) will be free for people below 150% of the poverty level, and scale up gradually from there. This will create a much smoother transition between expanded Medicaid and the marketplace plans. In 2020, someone moving from 138% of the poverty level to 139% of the poverty level would have been hit with premiums at 3.45% of their income (plus out-of-pocket costs) as they transitioned off Medicaid. In 2021, premiums for the second-cheapest silver plan won’t start until income exceeds 150% of the poverty level, and won’t exceed 2% of income until income passes 200% of the poverty level.

These changes are currently in effect for 2021 and 2022 only. I wrote more about this (and the effect on overall marginal rates for FIREd individuals) in another post.

Congress recently passed another round of COVID-19 stimulus, and President Biden has signed it into law. Part of this law is a change to the computation of the ACA premium tax credit. An update to my earlier analyses are therefore in order. The law changes the tax credits for 2021 and 2022. We are scheduled to revert to the previous tax credit amounts in 2023.

In a nutshell, the law does two main things for ACA marketplace customers: it increases the premium tax credit for everyone who previously qualified for one, and removes the cliff at 400% of the poverty level that prevented people slightly above this level from receiving any subsidy.

A graph of this difference is below, for a single person whose second-cheapest silver plan has a gross premium of $9,500 per year.

A few things stand out here:

1) There’s no difference below 100% of the poverty line. The cliff at this level remains. In expanded-Medicaid states, people in this range will typically be eligible for Medicaid coverage. In the remaining states, people in this range will often find health insurance to be completely unaffordable.

2) Between 100% and 400% of the poverty level, the tax credits are a bit bigger than they were before, almost $1,500 larger at some income levels. This includes lowering the net premium to $0 for people between 100% and 150% of the poverty level.

3) Above 400% of the poverty level is where things can be really different. Under prior law the premium tax credits cut off abruptly at this income level. The older you get, the more your unsubsidized premiums will be, and the steeper this cliff was. The new law smooths out the curve significantly. The subsidies still phase out at higher incomes, but it is now a gradual decrease rather than a sharp cliff.

What about the marginal rates?

One thing that I think continues to be overlooked in the retirement tax planning space is how the phase-out of premium tax credits affects marginal tax rates for people who purchase health insurance from the ACA marketplace. This phase-out adds a rather significant amount to the marginal rates, and this can in turn affect decisions workers make about whether traditional or Roth retirement contributions would be more advantageous.

The graph below plots the marginal rates under prior law just from ACA premium tax credit phase-outs, compared to the new 2021 law.

The blue line is the same as from my earlier post about this topic. From 100-133% of the poverty level the net cost of the second-cheapest silver plan (the “applicable percentage”) was formerly a flat 2.06% of MAGI, so that’s the marginal rate we saw. From 300-400% of the poverty level the applicable percentage was fixed at 9.78% of MAGI, so that again was equal to the marginal rate.

Between 133-300% of the poverty level, the applicable percentage gradually increased from 2.06% of MAGI to 9.78% of MAGI. This increase caused the marginal rate to actually be higher than 10%, because as your income increased the new applicable percentage that you’d pay for your health insurance was applied to your entire income (not just your marginal income).

The red line shows the marginal rates that arise from the new law. Notice the new 0% applicable percentage below 150% of the poverty level, resulting in no marginal tax from the subsidy phase-out in this range. The new law also creates lower marginal rates between 150-300% of the poverty level, as the applicable percentage is increasing a bit slower than before.

Above 300% of the poverty level we see a different story. The red line is actually higher than the blue line in this range. Instead of having a fixed applicable percentage between 300-400% of the poverty line, the new law has the applicable percentage gradually increase here. This has the effect of pushing the marginal rate up above the applicable percentage in this range, just as we’ve already seen elsewhere.

Once we exceed 400% of the poverty level, the new law fixes the applicable percentage at 8.5% of MAGI. This 8.5% number is the marginal rate we see up until the credit phases out based on the cost of your insurance. Previously we had a marginal rate of 0% here because once you fall off the cliff your health insurance would cost the same at 401% of the poverty level as it would at 500% or 600% of the poverty level. Under this new law that would no longer be the case. This makes the ACA marginal rates now apply to higher income levels than before.

Conclusion

We can see from the first graph that people at most income levels will be paying less for health insurance through the ACA marketplace in 2021 than they would under the rules in place previously.

We can see from the second graph that the marginal rate paid toward insurance premiums will also go down for people below 300% of the poverty level, while it will go up for people above 300% of the poverty level.

For people still in the accumulation phase, this might be a good time to re-evaluate your retirement account contribution decisions. If you’re targeting an income below 300% of the poverty level while you’re on the ACA, traditional contributions may look like a slightly better deal now than before, and Roth is looking a bit worse. The opposite is true if you’re expecting an income above 300% of the poverty level.

On the other hand, this new law is only set to be in effect for two years. If it is allowed to sunset, we’ll revert to the previous rules, and changing your long-term plans based on this will prove to be a mistake. If on the other hand this change proves politically popular, it could be extended beyond 2022 and in fact remain in place for some time. You’ll need to use your own judgement to decide which of these outcomes seems more likely and plan accordingly.

I spend perhaps a bit too much time optimizing my financial life, particularly the tax side of things. I make plans, learn new information, revise those plans, and repeat.

One example of this is around tax planning for early retirement. One basic strategy discussed in the FIRE community is to utilize a Roth conversion ladder to access retirement funds before the standard age. Another strategy is to harvest capital gains up to the top of the 0% bracket for this type of income. For a long time my plan was basically to combine these two: do Roth conversions up to the standard deduction, and also harvest as many tax-free gains as possible.

In the past year a couple of things have caused me to refine that plan.

First, when I did some more in-depth research into the effect of income on ACA subsidies, I realized that the “tax-free” capital gains income wasn’t so free after all. Where before I had planned to accelerate quite a bit of capital gains income into the near future, after that I decided to put that off until we’re no longer subject to the ACA acting as an additional tax on our gross income. We set a lower target income for ourselves, at 200% of the poverty level (to qualify for ACA cost-sharing subsidies) rather than the 0% capital gains threshold.

As a side effect of this ACA research, I realized that for families with kids, the 0% threshold for regular income actually extends quite a bit higher than the standard deduction because of the child tax credit. While we maintain our plan to withdraw spending cash from our taxable accounts before dipping into retirement accounts, now any additional room for income below our goal would come from Roth conversions rather than capital gain harvesting.

The second thing that changed our plans was being unexpectedly enrolled in Medicaid in December when we tried to sign up for an ACA plan for our first year of FIRE. While we projected an income well above the 138% of poverty level threshold for this program on an annual basis, we learned that Medicaid actually looks at your ongoing, monthly income to determine qualification. A one-time piece of income, such as the deferred compensation payment I received this month from my former employer, does not count at all toward this purpose.

Our experience with Medicaid has so far been mostly quite satisfactory, and so we’re now in no hurry to realize income in a way that would disqualify us from that.

Coronavirus hits

Fast forward to this March. The whole world has been turned upside down due to the novel coronavirus pandemic. This has created a lot of difficulties for a lot of people, but it also creates some opportunities as well.

With the stock market’s steep decline, this has created the opportunity to do some rebalancing in taxable accounts that may have been too cost-prohibitive before the pandemic.

Exiting employer stock

One of the first changes I made was to sell the rest of the stock I had been holding onto from the employer I left nearly six years ago. I joined that company prior to its IPO and so the shares had extremely low basis compared to their current value.

I had been gradually selling that stock off in the intervening years, but still had a pretty good chunk of it. The amount of unrealized capital gains I had embedded in that stock was high enough that selling it off in the near future didn’t fit into the plan, as much as I would have liked to diversify.

The market drop created an opportunity to do just that. Some of the index funds I had purchased in the past couple of years were now underwater. I was able to sell my old employer stock for a gain and also harvest an equivalent loss from index funds, causing no net change in our income for the year.

Optimizing foreign tax credit

One other consideration I had been looking at was how to get our foreign tax from dividend income below $600 per year. I had built up our portfolio using Bogleheads’ very well-thought-out principles of tax-efficient fund placement. This analysis suggests putting your international stock allocation in a taxable account as a first priority. This is because the foreign tax credit often makes international funds one of the most tax-efficient investments to hold in taxable form.

While I was working in a medium to high tax bracket this advice worked out wonderfully. The credit I got to claim against foreign taxes withheld from my index funds largely made up for the US taxes I would have otherwise paid on these dividends, and then some.

What I found as my taxable international investments grew is that once the foreign tax paid rises above $300 (or $600 for joint filers), you need to file Form 1116 with your taxes in order to compute the credit, rather than being automatically able to claim the full amount of foreign tax paid.

In higher income brackets this form, while a hassle to complete, quite often results in a credit equal to the amount of foreign tax paid. As a lower-income retired person this is much less likely to be the case. Therefore I had a goal to shift part of my foreign stock allocation from taxable to retirement accounts in order to avoid needing to file this form in future years.

Like with the employer stock, the amount of unrealized capital gain we had in these funds prior to coronavirus made selling these a goal that I expected to chip away at over several years. The market drop created an opportunity to sell enough of this for a loss (offsetting the employer stock) that our foreign tax amount should now be comfortably below the $600 threshold for the foreseeable future.

Minimizing dividends

Okay, so that was two big chunks of stock I didn’t want anymore that I was able to get out of with minimal tax consequences. Now what to buy? US stock is what I arrived at. It’s the next big asset class in the Bogleheads’ tax-efficiency hierarchy, and the 0% dividend and capital gains tax seems to make this tax-efficiency advantage hold true even and especially at lower income levels.

A total market fund like VTSAX might be the obvious naïve choice here, but in the end it isn’t what I selected. The reason lies with the earned income credit. This credit can provide pretty substantial funding to lower-income families who work, especially those with kids at home. See the chart below for an illustration of this. Our family recognized about $4,000 of earned income last year aside from the corporate job I left last year, which with two kids might be worth around $1,000 in tax credits.

There’s a catch though. This credit was designed to apply to the working class, not retirees living off their investments and also working the odd job here or there. As such, there’s a hard cutoff at $3,650 of annual investment income. Go above this cutoff by even a dollar and no earned income credit for you.

VTSAX tends to pay dividends in the ballpark of 2% of fund value. This means that someone with an all-VTSAX taxable portfolio will be disqualified from the earned income credit on dividends alone as the value of this portfolio approaches $200k. Our taxable portfolio is worth quite a bit more than this. While we do intend to spend it down over time as our first priority for liquidation in early retirement, we’re very likely to still have more than $200k in there by the time our kids are too old to qualify for the earned income credit.

I spent some time looking through Vanguard’s rather extensive lineup of index funds and found a promising solution: VIGAX, Vanguard’s Growth Index Fund. This index basically looks at the half of large US corporations that are considered “growth” companies. The other half are “value” companies tracked in another Vanguard index fund, VVIAX. So-called “growth” companies tend to reinvest their earnings back into growing their businesses rather than paying dividends. The result is VIGAX paying roughly 1% of its value in dividends, half of what VTSAX pays.

Buying VIGAX in a taxable account therefore doubles the amount of stock you can own and still potentially qualify for the earned income credit, when compared to owning VTSAX. Purchase a similar quantity of VVIAX in your retirement accounts to balance it out and you’ll still tend to track the broad market pretty well.

Even by going this route we’re several years out from when we might potentially qualify for the earned income credit, and if we hit another long bull market it may never happen, but the possibility creates a nice margin of safety to help us out if the market falls farther from here.

Stimulus payment

The stimulus check being sent out to most Americans this week is all over the news. Our income was a bit too high in 2019 to qualify for one of the immediate payments, but it will be much lower 2020. The way the law was written, the payment is a refundable tax credit against your 2020 taxes, with an advance payment given to those whose 2019 income was low enough to have qualified for that credit if it had applied last year. Come next spring we should be getting a $3,400 windfall in our tax refund.

Conclusion

This post has been about some of the ways we’re trying to make the most of this pandemic in a financial sense. What are some of the things you have been doing? I’d love to hear about it in the comments.

Finally, we consider ourselves extremely fortunate to be in a position to not need to fear much for our income in a time when so many businesses have scaled back operations or closed entirely. We are trying to pay it forward. I contributed quite a bit to a donor advised fund over the past couple years at higher incomes, and now has been a good chance to distribute that cash. We’ve made a couple of pretty sizable donations to the nearest food banks, as they struggle to feed the hordes of newly unemployed folks in our community. We’ll probably do a few more like this before the pandemic subsides. Please consider what you can do to help us all get through this.

If you asked me last year what I expected to be doing during the spring of my first year of FIRE, “hunkering down at home for an indefinite period in order to ride out a global viral pandemic” would not have been anywhere near the top of my list. And yet, here we are.

As of last week our governor ordered everyone to stay home as much as possible. “Essential” businesses may stay open and their employees can go to work as usual. The definition of “essential” is a bit broad for my taste (is take-out sushi really a necessity?), but it’s not too outrageous. Most people seem to be doing a pretty good job of complying with the orders.

This has been a wild time in so many ways. Schools are closed. Kids are home. So are most office workers. Nobody can buy hand sanitizer. Toilet paper and flour are precious commodities. Normally-vibrant business districts near my home are a virtual ghost town. Many of the restaurants have signs in the window proclaiming “YES WE ARE OPEN BUT ONLY FOR TAKEOUT,” but many (most?) retail businesses have gone dark.

Pretty much everything I do on a regular schedule has been cancelled. This includes three different volunteering gigs and a few recurring social engagements. In their place are the occasional video chat with friends and family, near and far.

The bus system is still running. In order to protect the drivers they stopped charging fares, blocked off the front section of the bus, and everyone is required to board through the back door unless they need to use the wheelchair ramp in front. I haven’t been on a bus in weeks though. From the nearly-empty buses I see going through the neighborhood it seems that most people are staying off if they can for the safety of themselves and others.

Residents are encouraged to go outside for walks or runs, but everyone must maintain a six-foot distance from anyone outside their household. Sometimes this is hard to do. I enjoy walks but find myself crisscrossing the street pretty often if someone is approaching from the opposite direction. If there’s someone walking in the opposite direction on the opposite sidewalk too, I just walk down the middle of the street for a bit. Vehicle traffic has slowed to a trickle of its usual volume so this is pretty safe to do.

The personal finance side of things has been interesting. Our net worth has gone down rather significantly, of course, but I’ve been pretty calm about it. I took a couple of opportunities to rebalance from bonds into stocks on the way down to maintain our predetermined asset allocation. Having a plan in advance really helps!

I’m thankful that our problems are relatively minor in the grand scheme of things. We haven’t lost an essential source of income. We’re at low risk for the disease in our house. We’ll get through this just fine. Not everyone will be so lucky. Let’s all do what we can to protect and enhance our communities during this time.

Being newly FIREd in August, this open enrollment season was my first experience with purchasing health insurance through our state exchange. I chose to maintain COBRA coverage through my previous employer through the end of 2019. We had already gotten most of the way toward our out-of-pocket maximum on that plan earlier in the year, and I felt it was unwise to start all over on deductibles with an ACA plan for the last few months of the year even if the premiums would be a bit lower.

When November 1 came around, I was all prepared. I had a letter written about what I expected my income to be in 2020, a set of financial statements all ready to support my estimates, and I got it all submitted the first day of the open enrollment window.

Children in Washington in a family of four are put on Apple Health (our state’s Medicaid program) up to a household income of $6,802 per month (more than $81k annually). Meanwhile adults in that same family are only eligible for Apple Health up to an income of $2,961 per month (less than $36k annually).

I submitted an estimate for 2020 income between these two numbers, which should result in my wife and me on a paid ACA plan and my kids on Apple Health.

All looked well at first. The system let me sign my wife and me up for a subsidized ACA plan, put my kids on Apple Health, and I received insurance cards for everyone for the upcoming year.

A few weeks ago I received a notification that they needed confirmation of my income for the last 60 days from two companies: the employer I left in August, and also the company I spent three days with as a background actor. At that point I had not worked for either organization in the past 60 days. I had collected a letter confirming termination of employment from my corporate job before I left, so I sent that in plus all my pay statements for the acting gig and crossed my fingers that this would satisfy the bureaucrats.

Spoiler alert…it didn’t.

Two weeks later they sent me a notification that they had not received the requested documentation in the required timeframe and so my sons would have their health insurance canceled effective at the end of the month.

Needless to say, I was displeased with this. In response I (gasp) made a phone call. After explaining the situation and waiting on hold for about half an hour while they looked things over, they told me that they had verified my income based on the documents I had submitted, and that my sons should be back on Apple Health.

Fast forward to this morning and I received an email notification from the exchange, with official written documentation of the new change in our status. I logged in to look it over and discovered that not only were my sons added back to Apple Health, but my wife and I were as well! Something the phone representative did must have bumped our estimated income below the threshold, and they didn’t see fit to mention “and oh by the way we’re cancelling your private insurance and moving you to Apple Health.”

Since it’s a holiday I’m not trying to call back now, but you can bet I will be doing so first thing in the morning. Here’s hoping I can get everything resolved before the new year rolls around.

IMPORTANT UPDATE: Congress has changed the ACA premium subsidy amounts for 2021 and 2022. The marginal tax rates resulting from the phase-out of these subsidies have also changed. See this post for a graph comparing the old marginal rates with the new marginal rates. In a nutshell, the rates have gone down for incomes below 300% of the poverty level, and have gone up at higher incomes. The basic premise behind the post below still applies.

ORIGINAL POST BELOW…

In a recent thread on the MMM forums, there was a discussion about how the phase-out of ACA premium subsidies can act as a second parallel tax system to the standard federal income tax. I had always been aware of this in theory, but had previously dismissed it as a pretty minor factor for planning because the percentage of your MAGI you’ll pay for insurance after subsidies is fixed at a relatively low rate (ranging from roughly 2% of MAGI at the low end of the income scale to a bit less than 10% at the upper end of the subsidy-eligible range).

What I failed to consider was that as your income increases and the percentage of income you owe for the reference insurance plan also increases, this new percentage is applied to your entire income, not just the marginal income. This causes the marginal rate of subsidy phase-out to be greater than the percentage of MAGI now owed. In fact in many cases the marginal rate is in excess of 15%!

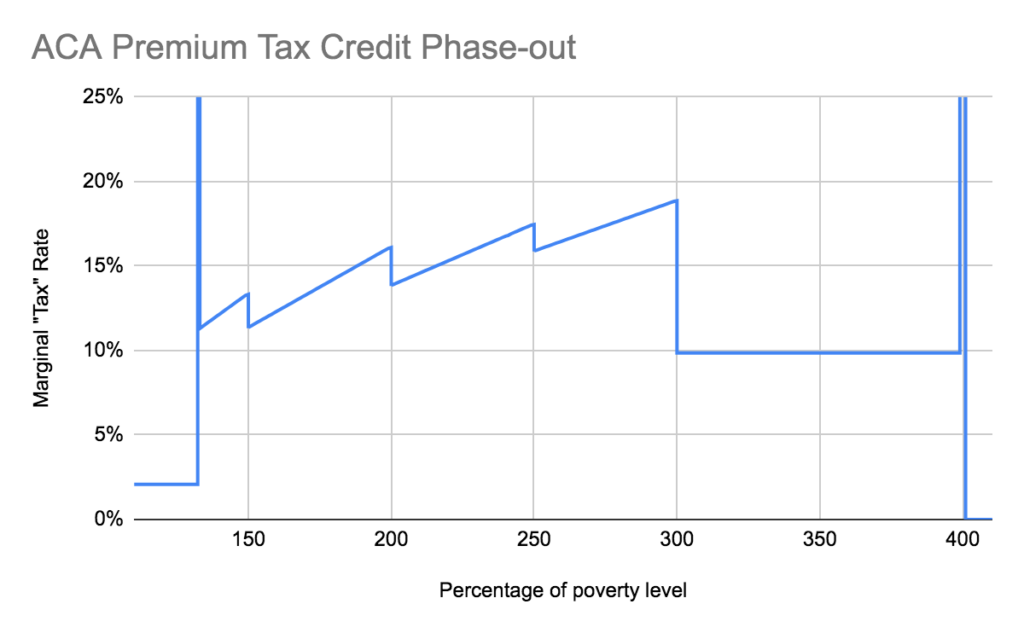

See the graph below for how this works.

Those big vertical lines represent cliffs at 133% of the poverty level (where there’s a sharp jump from 2.08% of MAGI to 3.11% of MAGI) and at 400% of the poverty level (where premium subsidies go away completely). Between the cliffs there’s a pretty big range where the marginal rate is right around 15%. Above 300% of the poverty level the applicable percentage of income is fixed at 9.86%, so that’s also the marginal rate that applies in this range.

How does this look when added on to the standard federal income tax brackets in early retirement?

Example 1: Single person

Let’s start with a pretty simple example, of a single person using the Roth conversion ladder to access their IRA funds during early retirement. All of their income is generated using this method. They claim the standard deduction and aren’t eligible for any tax credits besides the ACA premium assistance.

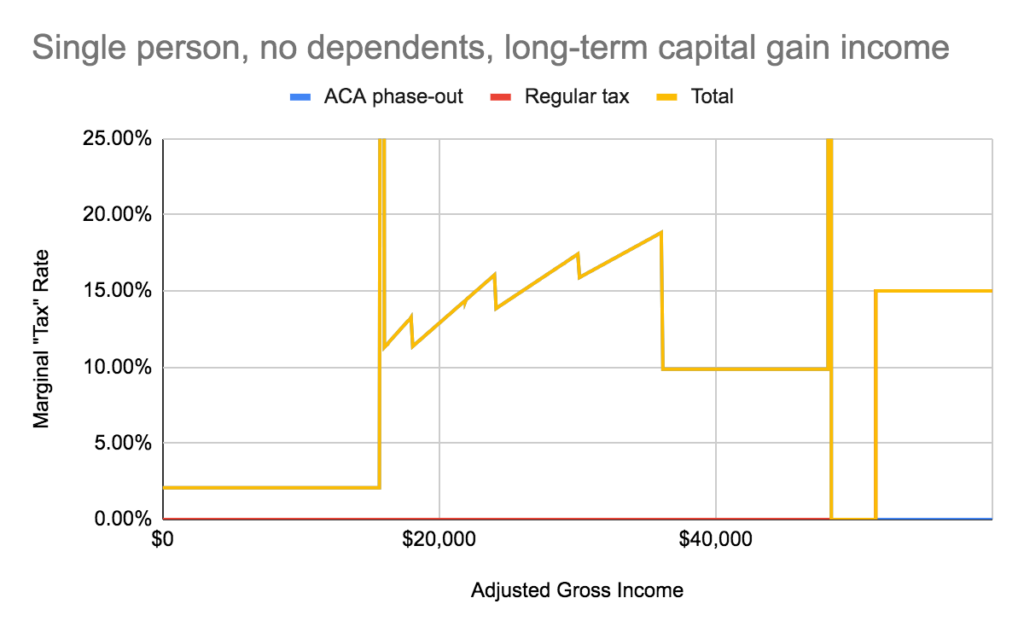

The blue line in this graph is exactly the same as in the first graph, representing the marginal rate for phase-out of the ACA premium tax credit for a single-person household.

The red line is federal income tax: 0% below the standard deduction, then a 10% bracket, 12% bracket, and 22% bracket. The yellow line is the sum of the two. To the right of the subsidy cliff the blue line goes to zero, so the red and yellow lines are identical at that point.

What we can see from this graph is that the total marginal rate for this individual is in excess of 20% for the entire ACA phase-out range, and in excess of 25% for a large chunk of it.

How about a single person drawing down their taxable investment account, getting all their income from dividends and long-term capital gains?

In this case the red and blue lines are hardly visible at all. During the ACA phase-out range the tax rate for long-term gains is 0%, so the yellow line overlaps the blue line. After that there’s no more ACA subsidy to phase out so the yellow line overlaps the red line.

I think this graph helps rebut the somewhat common question about whether Roth contributions make sense when taxable investments have a 0% income tax rate at lower income levels. If it’s tax-free either way, why tie the money up in a Roth IRA, right?

Well, if you’re planning to take ACA subsidies, it’s not tax-free either way. You’ll be paying for those “tax-free” capital gains in the form of lower ACA tax credits, while withdrawals of your Roth principal don’t count toward your MAGI and therefore don’t affect your ACA tax credit in the slightest.

The graph of capital gains income above is basically the same for other family sizes: only ACA phaseouts count toward the marginal rate in the phase-out range, then there’s a period of truly zero tax after the ACA cliff, then the 15% capital gains rate starts to apply later. The income levels stretch out based on family size, but the general form of the graph stays the same.

Example 2: Family of four

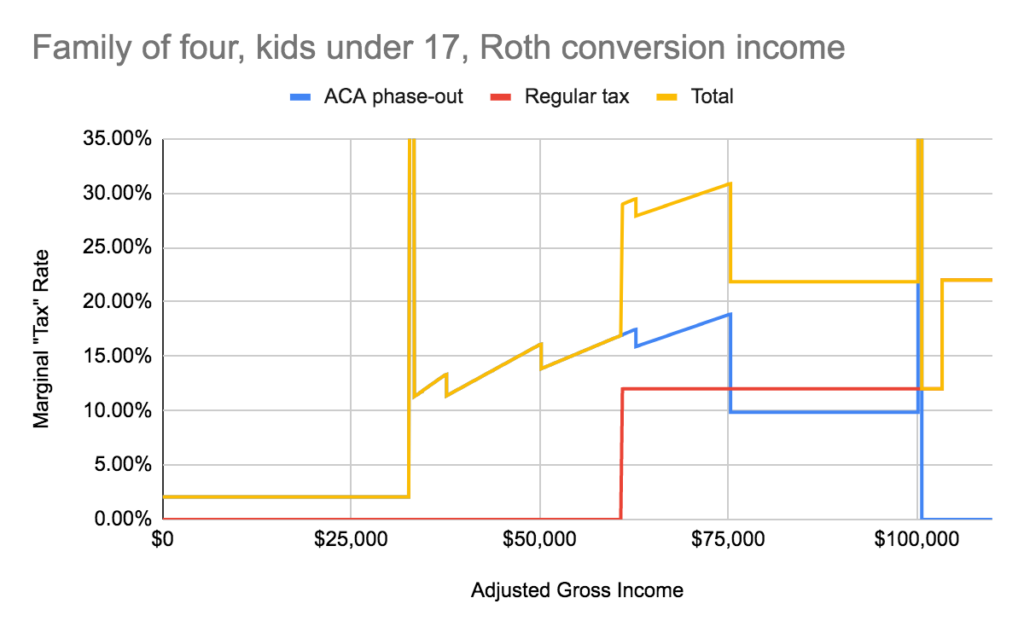

Now we’ll look at a family of four: a married couple with two kids under the age of 17. All of their income comes from Roth conversions. They claim the standard deduction, child tax credit, ACA premium tax credit, and nothing else.

This family has a pretty big range (up to nearly $61,000 in gross income) where the child tax credit erases their federal income tax liability, so only the ACA phase-out contributes to their total marginal rate. After that it looks pretty similar to the single-person example, with total rates around 30% up to 300% of the poverty level, then dropping down to 22% until the subsidy cliff.

What happens as the kids grow up? Once they hit age 17 they’re no longer eligible for the $2,000 child tax credit, but as long as they remain dependents of their parents there’s a $500 “credit for other dependents.” If both kids fall into this situation, it looks something like this:

This is starting to look a lot more like the graph for a single person. Not quite all of the ACA subsidy phase-out range has total marginal rates in the 20-30% range, but it’s pretty close.

Fast forward a few years, the kids finish school, earn their own money, and stop being tax dependents. What happens then? The parents will still be paying taxes as a married couple, and will now be using the two-person household poverty level for their ACA subsidies.

This graph has an x-axis at the same scale as the previous graphs for a four-person family. Notice that the ACA phase-out range has moved over to the left and compressed into a smaller range. This couple will need to sharply reduce their income if they want to keep paying the same amount for health insurance as before their children moved on, and maybe to keep getting any ACA subsidies at all. This is happening at the same time as they’re getting older and facing higher premium costs if they were to lose their subsidies.

Conclusions

I know that this sequence of graphs has caused me to reconsider my family’s long-term tax strategy. I had previously thought it best to focus on spending down taxable investments early on in FIRE, then focus more on Roth conversions later on.

Now that I see how the child tax credit gives us a pretty big amount of space where Roth conversions are taxed the same as capital gains, but only until the kids turn 17, perhaps accelerating some of those Roth conversions would make sense in order to build up some more basis in those accounts and allow us to more easily reduce our income when we have no more dependents to declare.

I’m also starting to think the standard advice in the FIRE community to prioritize pre-tax retirement accounts over Roth while in the accumulation phase may be misguided. The assumption is that someone who spends a fraction of their income while working will be very likely to retire into a lower tax rate. As we can see in these graphs that isn’t such a sure thing when you also consider the ACA subsidy phaseout as part of your marginal tax rate in retirement.

Someone earning enough to hit the 35% bracket during their career would still be seeing a pretty definite win by deferring a bunch of taxable income until retirement. For people even in the 24% bracket while working, we can see plenty of relatively low retirement incomes where you’ll be paying more than that.

Of course if you would rather buy insurance from a private carrier instead of relying on Medicaid you’ll need to come up with some level of income that counts toward MAGI in retirement. But maybe the best thing for most folks with relatively normal salaries to do is to save just enough pre-tax to hit the very low end of the ACA subsidy range each year in retirement and go with Roth for the rest.

What do you think? I’d love to hash this out more in the comments.

One of the great things about being FIREd is having the ability to take time to try new things. Last week I had the opportunity to try my hand at being a background actor (aka “extra”) on a new TV show.

Going into it, I had no idea what to expect. I found out about the opportunity from a friend of mine who saw the casting call posted to Craigslist. Neither of us had any previous experience with this sort of thing. We both responded saying we were interested and available. She was called in to film on one day for a scene in a bar, and I was called in to film on three days: one day filming in a gymnasium scene and two days filming outdoors in a park.

The first day was pretty disorganized. They called a bunch of us in bright and early, got us set up with our costumes for the scene, and then we sat outside for about eight hours before we actually had to do anything. There was an assistant director who was our point of contact, and he kept telling us we would be needed in an hour or so. They must have had a bunch of things run behind schedule, as they didn’t end up needing us until the very end of the day.

When we were called in it was a pretty surreal experience. I had never been on a professional set like that before. There were lots of people involved, each with their own jobs. They would all do their thing to get set up for the next shot, perform the scene, reset everything back to the beginning for the next take, and repeat from there. I was pretty impressed by how well everyone seemed to work together.

The second day I went in was a bit more involved. At the beginning they had us consult with a wardrobe professional, handing out the costumes we were supposed to wear and having us try them on. They also had us spend a few minutes with hair and makeup artists to get us looking our best for the camera.

Once all that was done we headed to the set location in the middle of a public park. We were on camera much more that day. Not nearly so much sitting around waiting to be called in like the first day.

The filming was a bit challenging for everyone because the park we were in was underneath a flight path into the airport, so there was airplane noise interrupting things every couple of minutes. We got into a nice rhythm of setting things up during the airplane noise so that we were ready to go right away when it was over.

Another challenge was related to sunlight. It was cloudy when we started out shooting the scene, but later in the day the sun came out. This difference in light levels isn’t great for the continuity of the scene. Makes perfect sense when you think about it, but it’s something that I hadn’t considered before as just a viewer of TV shows. The crew brought out this big 20′ square shading device and set it up over our heads to make some shade and get the light levels down to about what they were when it was cloudy. Once again, I was impressed with how much everyone in the crew performed their different roles to keep things moving along.

That day was pretty tiring. We were there for about 12 hours, right until sundown. Then we had to show up again before sunrise the next day for the final day of filming. That morning they only needed us for a few shots, and we were done with our scene by lunchtime.

All in all, this was a very positive experience for me. Besides the opportunity to see how a TV show is made behind the scenes, I also met a bunch of interesting people. Most of my fellow extras were not new at it, and had even retained talent agents to try and find them as many roles as possible.

I don’t think there’s enough film work available in the Seattle area for anyone to make much of a real career out of acting here; it’s more something that people interested in it can do from time to time for a bit of extra cash if they have flexible jobs. I met a woman trained as a chef who works in sales, has been on a couple of reality shows, and aspires to have her own cooking show someday. I met a man who did web development for a few years before leaving that to become a juggler and pub trivia quizmaster, and who had made two appearances on game shows. There was a real estate agent who was also making his first appearance as an extra, and plenty of others each with their own story.

We all came together for three days working at minimum wage to fill out the background of a few scenes on a TV show. I think we did pretty well at it! It was fun to try once, and I can’t completely rule out doing it again in the future, but I’m also not going to scour the web for the next available opportunity. It started to feel a bit too much like work by the end, especially that last day with the pre-dawn start time.

Next year will be our family’s first experience buying health insurance on the individual market through our state’s ACA exchange. In 2019 there are four companies offering insurance in King County (home to Seattle, many of its suburbs, and nearly a third of Washington’s population): Ambetter, Kaiser Permanente, Molina, and Premera. Premera offers EPO plans, while the other three insurers are HMOs.

That’s this year. What about next year?

While the insurers aren’t actively selling their plans yet, they have all submitted proposals to the state insurance commissioner for the plans they would like to offer and rates they would like to charge. The commissioner has to review and approve these rates before the plans go on sale during open enrollment later this year.

I spent a little time looking through these proposals to see what’s in store for next year. All four of the companies currently offering individual insurance in King County plan to continue doing so next year. We’ll also see the addition of two more companies to the local exchange: BridgeSpan and LifeWise.

Keep reading for a company-by-company summary of the proposals for next year.

As someone who recently joined the ranks of the FIREd, I have plenty of options for how to spend my time. It’s pretty nice! While I’m confident that our savings should be enough to see us through the rest of our lives, I fully expect to come across some opportunities to do interesting things and also earn some money on the side.

My first thought when considering the impact a small side gig might have on our finances is that the self-employment taxes will be huge, and that the amount left over might not be worth the effort. As I found out, this is not necessarily the case for a FIREd family.

Example 1: Roth conversion ladder

Consider a retired couple with two kids living at home, spending $50,000 per year. They have essentially all of their savings in retirement accounts, and use the Roth conversion ladder to access this wealth prior to age 59½.

Their federal income tax situation, in a nutshell, looks like this:*

Adjusted Gross Income: $50,000 from Roth conversions

Standard deduction: $24,000

Taxable income: $26,000

Tax before credits: $2,742

Child tax credit: $2,742

Total tax (before ACA credits): $0

No income tax for this family. Not bad! This family buys their health insurance through their state’s ACA exchange. With an AGI of $50,000, the second-cheapest silver plan will have annual premiums of $3,225. They pay for these premiums out of their $50,000 budget.

Now consider what might happen if one of the adults in this family starts a small part-time business, bringing in a pretty modest $15,000 per year. They use this money to help pay their living expenses, reducing their need for Roth conversions by an equal amount. This business would expose the family to self-employment tax of 15.3% on the business income, but it also opens up a few interesting tax breaks for self-employed folks.

First, self-employed people can deduct the cost of their health insurance premiums. This deduction is calculated prior to AGI, similar to the treatment that people who get health insurance through their employer get to claim.

Self-employed people also get to deduct half the cost of their self-employment tax from their AGI, similar to how employees have their employer pay half their FICA taxes and this half never enters into their own personal income tax calculations.

The tax cuts that went into effect in 2018 introduced a new deduction for business owners: the 20% qualified business income deduction. This applies to business income that is not otherwise deducted from income, so the deductible half of self-employment tax and the health insurance deduction don’t count toward the income that is used for this deduction.

Finally, the fact that this family now has some work-related income makes them potentially eligible for refundable child tax credits and the earned income credit.

Let’s see how their taxes shape up now!

Roth conversion income: $35,000

Business income from Schedule C: $15,000

Gross income: $50,000

Deduction for half of self-employment tax: $1,060

Deduction for health insurance premiums: $2,679

Adjusted gross income: $46,261

Qualified business income deduction: $2,252

Standard deduction: $24,000

Taxable income: $20,009

Tax before credits: $2,022

Child tax credit: $2,022

Regular income tax: $0

Self-employment taxes: $2,120

Additional child tax credit: $1,716

Earned income credit: $1,099

Total tax (before ACA credits): $-695

That’s right, negative $695 of tax! Far from being an expensive proposition tax-wise, this self-employment activity unlocked tax credits that more than paid for the self-employment tax. The pre-AGI deductions from self-employment also increase their ACA premium tax credit by $546. That’s a total benefit of $1,241, even before taking into account the effect that this extra $15,000 of work income will have on their eventual social security benefits.

Example 2: Spending down a taxable account

The previous example looked at a family who was going with the Roth conversion ladder for 100% of their spending. Now let’s look at a family in a situation more similar to my own, starting out in FIRE with a taxable brokerage account that they want to spend down before moving on to tax sheltered funds.

Same family size and $50,000 spending as before. This time they take the full $50,000 from a taxable account: $10,000 of dividends and $40,000 from selling shares with an average basis of half the current market value, leading to $20,000 of long-term capital gains income.

They also do $20,000 of Roth conversions to prepare for future years when they’ll be relying on seasoned Roth basis for their Roth conversion pipeline.

Tax situation before starting a small business:

Roth conversion income: $20,000

Qualified dividend income: $10,000

Long-term capital gains: $20,000

Adjusted Gross Income: $50,000

Standard deduction: $24,000

Taxable income: $26,000

Tax before credits: $0

Child tax credit: $0

Total tax (before ACA credits): $0

Similar to the family living off Roth conversions above, the family in this example has no federal tax liability before starting their small business. Let’s see what happens afterwards with $15,000 of self-employment income.

As they’re still trying to spend down their taxable account, they keep withdrawing from their taxable savings as before, and save their full self-employment earnings in Roth retirement accounts. They reduce their Roth conversions by $15k to keep their taxable income pretty steady.

New tax situation:

Roth conversion income: $5,000

Business income from Schedule C: $15,000

Qualified dividend income: $10,000

Long-term capital gains: $20,000

Gross income: $50,000

Deduction for half of self-employment tax: $1,060

Deduction for health insurance premiums: $2,679

Adjusted gross income: $46,261

Qualified business income deduction: $2,252

Standard deduction: $24,000

Taxable income: $20,009

Tax before credits: $0

Child tax credit: $0

Regular income tax: $0

Self-employment taxes: $2,120

Additional child tax credit: $1,716

Earned income credit: $0

Total tax (before ACA credits): $404

In this scenario the family is ineligible for the earned income credit due to their taxable investment income. Anyone with more than $3,500 of such income is ineligible for the earned income credit. The additional child tax credit and the additional ACA credits still combine to more than annihilate the self-employment taxes.

This is a result I didn’t really expect when looking into the impact a side business would have on an early retiree’s taxes. I thought that surely the taxes would go up. In many cases, especially where kids aren’t involved, that probably would happen. But when you bring kids into the mix, tax credits meant to help low-income working families can help you too!

* All calculations in this post use tax formulas from 2018. Amounts in 2019 will differ slightly due to annual inflation adjustments in the tax code.

It has been a while! After opening this blog with a couple of posts four years ago, life got in the way and I never had the necessary combination of time, motivation, and ideas to write something new here…until now.

I FIREd two weeks ago and thought I’d dust off this blog to record some of my thoughts and experiences during this pretty big life transition. Will I make a long-term habit of posting here? Probably not! I’ve started personal blogs a few times before and have never made it to a dozen posts before fizzling out. That said, maybe now that I’ve let go of the day job and embarked on this new adventure I’ll come up with a nice variety of thoughts that I feel like sharing with the world.

I thought I’d start with some examples of how I’ve spent my time now that I’m out of the workforce.

My first day of FIRE was pretty mundane. I went to the dentist. My corporate dental plan goes away at the end of the month, so that was an opportune time to go in and get my mouth all poked and prodded and tidied up. On my way home from the dentist I stopped at a thrift store to pick up some clothes my son needed. Again, pretty mundane stuff, but it felt great to have the time to do both of those things without any rush imposed on me by an external work schedule.

One morning my wife and I did a scavenger hunt in our old neighborhood, full of cryptic clues leading us all over the place on foot. The neighborhood community center organizes the event every year as a fundraiser but we never actually found time to try it until now. We really enjoyed it!

On a Tuesday we went to a hike out in the mountains. It was a trail that tends to be packed with people on the weekends. We didn’t exactly have it to ourselves on a Tuesday, but it was rather uncrowded nonetheless. How nice to have the freedom to take a day and do that when the crowds aren’t there!

Last weekend I spent an afternoon helping some friends do some electrical wiring as part of a larger remodeling project they’re doing. This is something I have a bit of experience with from previous DIY projects. Lending a hand felt nice.

That weekend we also went to a beach park we had never visited before, just a short drive from our house. They were having a sand castle contest that day, which was fun to see.

One thing I’m really looking forward to during my retirement is having time to pick up new skills. The first one of these: home canning. This has been something I’ve wanted to learn for years, but never quite got around to it. When our CSA has given us too many cucumbers I’ve made refrigerator pickles, and when our apple tree at our old house produced a bunch of fruit we’ve filled our freezer with applesauce. The art of home canning always seemed like just a little bit too steep of a learning curve when we were also in the midst of all this produce to process.

Now we have an apricot tree. It’s much more prolific this year than the previous two years we’ve owned it. In fact it’s so prolific that a couple of branches broke under the weight of all the fruit! Rather than compost all those unripe apricots, we found a nice recipe for how to make jam out of them. It’s pretty delicious! We had enough fruit to make gallons of jam, too much to keep in our refrigerator. The time was right to finally get canning!

I read some online tutorials, bought a couple dozen Mason jars from Goodwill, got some new lids for them, and went to work. The result: 10 pints of delicious jam ready for the pantry, plus quite a bit that went straight to the fridge. As the rest of the apricots ripen, there will more where that came from! The cost is quite attractive too. With a free source of fruit, I can fill and seal a jar of jam for less than a dollar. The savings are sure to add up, especially given the number of apricots I see ripening outside and the number of peanut butter and jelly sandwiches we eat in our house.

That’s all for now. So long, and thanks for reading!