As I write this, we are almost halfway through the second year of health insurance being available to everyone on state exchanges regulated by the Affordable Care Act (also known as Obamacare). This law has not been without controversy or legal challenges. Regardless of your opinion on whether the ACA was a good idea, it is here and is likely to stick around for some time.

People planning to retire early in the US will likely find themselves buying health insurance from their state exchange until they become old enough to qualify for Medicare. These insurance policies can be subsidized for people with lower incomes. For early retirees who have some flexibility in how much taxable income they have in a given year, understanding how these subsidies work can become especially important.

There are two main types of subsidies available: premium discounts and cost-sharing subsidies.

Premium discount subsidies

Insurance plans on exchanges are grouped into the following “metal” levels:

- Bronze plans will pay for 60% of the average customer’s medical bills.

- Silver plans will pay for 70% of the average customer’s medical bills.

- Gold plans will pay for 80% of the average customer’s medical bills.

- Platinum plans will pay for 90% of the average customer’s medical bills.

In general, the higher metal levels will have higher monthly premium costs. The lower metal levels will have lower monthly premiums, but the deductibles and out-of-pocket expense caps will be higher because the plan is not required to cover as much of the cost.

People whose modified adjusted gross income (MAGI) is between 100% and 400% of the Federal Poverty Level who don’t qualify for Medicare or Medicaid are potentially eligible for premium subsidies. For reference, the 2014 FPL (used for computing premium subsidies in 2015) is $15,730 for a two-person household. This means that a two-person household with MAGI between $15,730 and $62,920 could qualify for a subsidy. Households outside this range will pay full price for all plans offered through the exchange.

Every state (and even different areas within the same state) will have different plans available at different costs. Because costs and options can vary from place to place, Congress decided to use the second-cheapest silver plan in your area as a baseline for subsidies you might receive.

The subsidy is designed to make this baseline plan cost a certain percentage of your MAGI after applying the subsidy. The percentage is a sliding scale ranging from 2% of MAGI for people between 100%-133% of the FPL all the way up to 9.5% of MAGI for people with MAGI between 300%-400% of the FPL. The subsidy amount is calculated by subtracting the applicable percentage of your MAGI from the full cost of the baseline plan. This subsidy amount can then be applied to any plan available on the exchange.

As an example, suppose Alice and Bob live in Seattle, are both 40 years old, and have a MAGI of $40,000. This amount is 254% of the Federal Poverty Level. Based on the sliding scale (source: Table 2 of the IRS Form 8962 instructions), a household with that income will be eligible for subsidies if the second-cheapest silver plan costs more than 8.17% of their MAGI, or $272.33 per month.

The Washington Health Plan Finder site lists 67 total plans available for them, of which 24 are silver plans. The second-cheapest of these silver plans has a premium of $507.12 per month. Therefore Alice and Bob would be eligible for a subsidy of ($507.12 – $272.33) = $234.79 per month. Whichever plan they pick, they can apply this $234.79 subsidy. If they choose the cheapest bronze plan (costing $387.68), the net cost after premium subsidy would be ($387.68 – $234.79) = $152.89 per month.

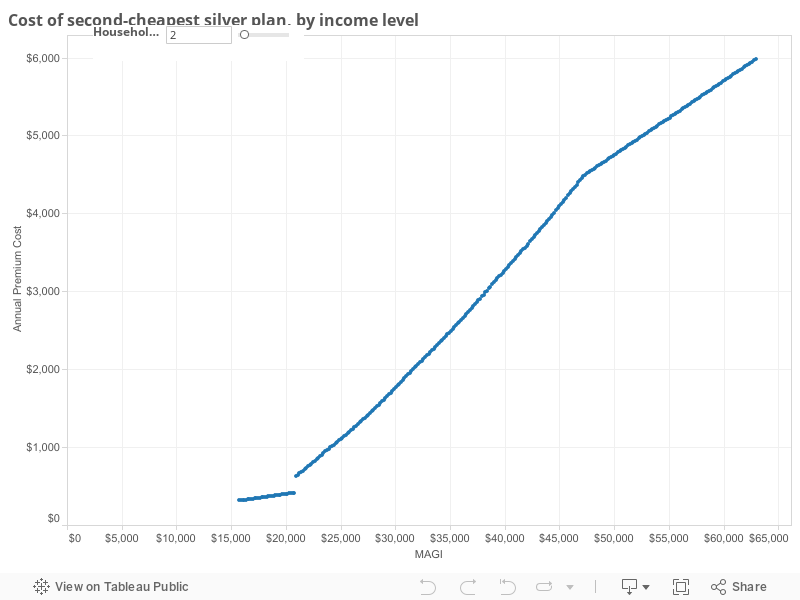

The chart below shows the relationship between MAGI and the net cost of the benchmark silver plan.

Cost sharing subsidies

In addition to the premium discount subsidies, there are also “cost sharing subsidies” available to households with MAGI under 250% of the FPL. These subsidies make silver plans (and only silver plans!) cover a higher percentage of your medical bills. The changes are as follows:

- Over 250% of the FPL, silver plans will pay for 70% of the average customer’s medical bills (normal amount).

- Between 200% and 250% of the FPL, silver plans will pay for 73% of the average customer’s medical bills.

- Between 150% and 200% of the FPL, silver plans will pay for 87% of the average customer’s medical bills.

- Between 100% and 150% of the FPL, silver plans will pay for 94% of the average customer’s medical bills.

As you can see, households that have MAGI under 200% of the FPL can get a plan that is basically as good as (or better than) a platinum plan, for the price of a silver plan.

Let’s look at what happens to the second-cheapest silver plan for Alice and Bob (40-year-old couple in Seattle) as their income changes.

| Income range | Annual deductible | Coinsurance percentage | Out-of-pocket maximum |

|---|---|---|---|

| Over 250% of FPL | $4,000 | 20% | $10,000 |

| 200%-250% of FPL | $3,000 | 20% | $8,000 |

| 150%-200% of FPL | $1,000 | 10% | $2,600 |

| 100%-150% of FPL | $400 | 10% | $1,000 |

Each income bracket down, the plan starts paying sooner and the annual “worst case” medical bills get lower.

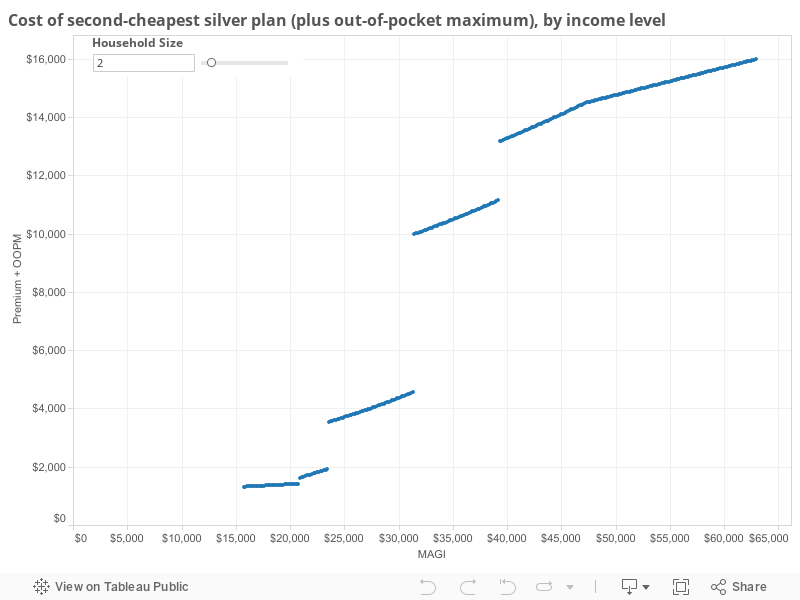

Here’s that same chart from above, but updated to include these out-of-pocket maximum values. Note that these values are just an example. Different plans achieve the required cost sharing percentages in different ways.

See the big jumps there? While the premium subsidy tapers off gradually as your income rises, that’s not the whole story. The premium is the minimum you’ll pay for your health care during the year if you don’t have any need to get help from a doctor at all. If you end up needing significant medical attention, even a short hospital stay can easily push a family’s annual cost up to the plan’s out-of-pocket maximum. As you can see from the chart above, this total cost function is not a smooth curve at all; there can be some very significant costs to moving from one cost sharing subsidy income bracket to the next.

Modified Adjusted Gross Income, defined

What is MAGI, anyway? It’s your Adjusted Gross Income (the number at the bottom of the first page of your Form 1040), modified as follows:

- Tax-exempt interest (from Form 1040, line 8b) is added.

- Certain untaxed foreign income is added.

- Any untaxed social security benefits are added.

Of particular interest to early retirees:

- Any wage or side business income increases your MAGI.

- Any interest, dividends, and capital gains in taxable accounts increase your MAGI.

- Any taxable Roth conversions increase your MAGI.

- Any taxable traditional IRA or 401(k) withdrawals increase your MAGI.

- Any tax-free Roth withdrawals do not change your MAGI.

- Any tax-free HSA withdrawals do not change your MAGI.

- Any tax-deductible HSA or IRA contributions decrease your MAGI.

- Itemized deductions (state tax, mortgage interest, charitable contributions, etc.) or your standard deduction do not change your MAGI.

Optimizing your income

This has been a lot of background information on the ACA so far. What do we do with all this information? How do you withdraw from your various retirement accounts to get the best deal on health care, while still having enough cash available to live a good life in retirement and also keeping your taxes low?

This is a hard problem with a lot of moving parts. The answer depends on your individual circumstances. The major things to consider are:

- How much do you plan to spend per year after you retire? What multiple of the FPL is this amount?

- When you retire, what types of accounts will hold your money, and in what ratios?

Depending on what types of accounts you will have, your MAGI may be the same as your spending. It could also be higher or lower. You may even have the ability to pick a target MAGI in advance and make it happen for a given spending level by moving money from different places.

Withdrawals from taxable accounts can affect your MAGI in various ways depending on which shares you sell. If you sell highly appreciated shares (say, shares that have quadrupled in price since you bought them), each dollar you take out of the account might add 75¢ to your MAGI. If you sell shares that have only gone up by 5% since you bought them, you might only add 5¢ to your MAGI for every dollar you withdraw. This quality can give you some tremendous flexibility in your retirement.

If you’re planning on doing the Roth conversion pipeline strategy, be aware that Roth conversions after retirement will generally increase your MAGI dollar for dollar. Five or more years down the line when you withdraw the money, these withdrawals will not add to your MAGI at all.

HSA withdrawals (when used to pay qualifying medical expenses) also do not add to your MAGI at all.

Given all of this, pick a target retirement MAGI for yourself that can meet your desired spending targets and is achievable with the funding sources you have. You may start retirement by selling less-appreciated shares from your taxable account to pay your expenses, while having most of your MAGI come from Roth conversions building up your pipeline for later. Then once your taxable account only has more highly-appreciated shares, you may decrease your Roth conversions as your capital gain income increases.

Let’s go back to Alice and Bob. They are a 40-year-old couple that just retired this year. They have $250,000 in a taxable brokerage account, $50,000 in an HSA, and $500,000 in a traditional IRA, for a total stash of $800,000. They plan to withdraw $30,000 each year, a little bit less than a 4% withdrawal rate. This withdrawal amount happens to be just under 200% of the FPL. They plan for $30,000 to be their MAGI target as well so they can qualify for the second-highest cost sharing subsidy.

For the first few years, Alice and Bob will withdraw $2,500 of qualified medical expenses from their HSA, and the remaining $27,500 from their taxable account. They will start selling least-appreciated shares to minimize capital gains. Each year they will convert ($30,000 – capital gains) from their traditional IRA to Roth IRA to start their Roth pipeline. Assuming historically typical investment growth, their taxable account should last at least ten years, with 12-15 being more likely. By the end of this time they should have enough seasoned Roth principal to start withdrawing $27,500 from that account tax-free each year and converting a full $30,000 from traditional. They will continue with this until they turn 65 and are eligible for Medicare.

What if Alice and Bob want to spend $35,000 per year? They might not be able to sustain that rate of spending while keeping their MAGI under $30,000. In that case they can do extra Roth conversions and harvest some extra capital gains for the first couple of years of their retirement, paying a little bit of extra tax and sacrificing ACA subsidies during years when they’re still relatively young. By realizing extra income in the beginning, they raise the cost basis on their remaining taxable shares and build up some extra Roth principal. This will allow Alice and Bob to sustain a situation of (MAGI < spending) for the future years when they are older and would benefit more from higher health insurance subsidies.

A note on Health Savings Accounts

HSAs are a great account for early retirees. This has been covered elsewhere. Some of the great, unique features include the ability to withdraw the money tax-free as long as you haven’t yet withdrawn more than your total medical expenses since you opened the account, as well as the ability to keep contributing to the account after you retire and no longer have any earned income. These properties can make the HSA a great backup source of retirement income in years where you need a little bit of extra cash but have almost gone to your maximum target MAGI for the year.

Despite this, you should not plan to contribute to an HSA in a year where you also qualify for cost-sharing subsidies under the HSA. To meet the required coverage percentages for these subsidies, insurance companies often have no choice but to lower plan deductibles past the point where the plan would qualify as an HDHP that allows you to make HSA contributions.

However if you find yourself in the situation of purposely having a high MAGI for the first few years of retirement to enable lower-MAGI years later, don’t forget about the possibility of making HSA contributions. These contributions can help you in the current year by reducing your regular income (from Roth conversions, etc.) dollar for dollar while helping you in the future by allowing you to shelter some of your taxable money in the HSA where it will never count against your MAGI again.

A note on mortgages

Much ink has been spilled about the relative benefits of paying off your mortgage early versus investing that money in the market to get a higher expected return. While you’re still in the accumulation phase, the math generally favors making only the required payments on the loan and no more. Be aware that if you continue having a mortgage during the first part of your retirement, you will likely need to withdraw more from your various accounts to make the mortgage payments than if you had paid off the loan before retiring. This will likely cause you to have a higher MAGI than if you had no mortgage, which could in turn cause you to have higher health care expenses. Remember to consider this when deciding whether to carry a mortgage during retirement.

A note on Medicaid

I haven’t mentioned Medicaid much here. Medicaid is administered on a per-state basis with financial assistance from the federal government. As part of the ACA, states may choose to expand Medicaid to households with MAGI up to 138% of the FPL, in exchange for additional federal funding. The subsidies discussed above are only available to people whose income is too high to qualify for Medicaid in their state. Thus the subsidies for households between 100% and 138% of the FPL are only available to people who live in states that chose not to expand Medicaid.

The quality of coverage and selection of doctors available under Medicaid varies from state to state. While the program is intended to provide complete health care to lower-income individuals and families, many people report that the overall quality of care is not as good as what is available under privately-purchased health plans. Consider this when planning your retirement income, to ensure that your MAGI never drops below the Medicaid cutoff if you do not believe Medicaid provides good enough care in your state.

Final thoughts

While the ACA adds plenty of complexity to early retirement planning, it also removes a large source of uncertainty from the expense side of the equation. No longer do people need to remain working a job for the sole purpose of ensuring continued access to health care in the case of pre-existing conditions. Love it or hate it, the ACA is here and you should plan for how it will fit into your individual situation.

If you have any other thoughts about how to use the ACA in retirement planning, please comment below! Comments about the politics behind the law are off topic and will be removed.